Is Regulatory Overload Pushing Insurance Brokers Out of Business? A Critical Look at the Data

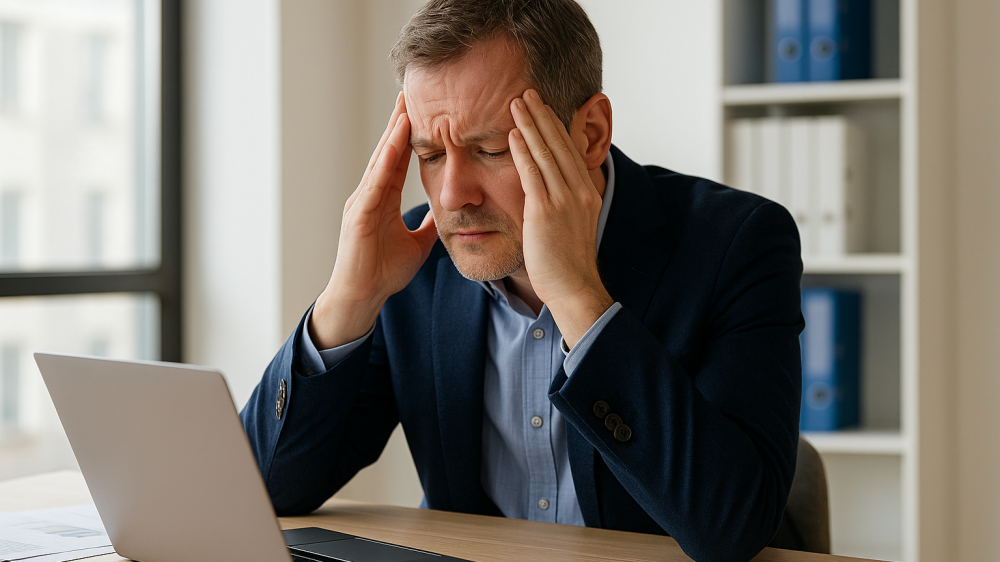

If you're an insurance broker, you're likely feeling the squeeze. A tidal wave of new rules, documentation requirements, and compliance checks isn't just a nuisance—it's a fundamental threat to your business model and your ability to serve clients effectively. A stark new survey from the Bundesarbeitsgemeinschaft zur Förderung der Versicherungsmakler (BFV), in cooperation with AssCompact, quantifies this growing crisis. The key finding is alarming: over one-third (35.8%) of surveyed brokers have seriously considered leaving the profession due to the sheer weight of regulation.

This isn't just a German phenomenon. Brokers and financial advisors worldwide, from those navigating Germany's PKV (private health insurance) and GKV (public health insurance) systems to those advising on U.S. Private Health Insurance, Medicare, and Medicaid plans, face similar compliance complexities. The core challenge is universal: balancing essential consumer protection with a regulatory burden that can stifle the very advisory services it aims to protect.

The Time Drain: How Many Hours Are Lost to Paperwork?

The survey of 565 intermediaries paints a clear picture of the time cost. This isn't about minor administrative tasks; it's a significant weekly commitment that directly cuts into revenue-generating activities:

- 45.7% of brokers spend 6-10 hours per week on regulatory tasks.

- 25% spend even more, with some exceeding 15 hours weekly.

- Per client meeting, up to 60 minutes can be consumed by mandatory documentation and administrative duties.

This massive time investment erodes economic efficiency and, most critically, diminishes the quality and quantity of face-to-face client advice. When you're buried in GDPR forms, ESG preference questionnaires, and compliance checklists, you have less time for the deep, personalized consultation your clients need—whether they're choosing a complex PKV tariff or comparing Medicare Supplement plans.

Small Business, Big Burden: A Skewed Competitive Landscape

The regulatory avalanche hits smallest the hardest. A overwhelming 90.3% of respondents agree that small and medium-sized brokerages bear the brunt of this burden. Unlike large corporate agencies or direct insurers, independent brokers often lack the dedicated legal departments and administrative staff to manage this load efficiently. This creates a significant market distortion, tilting the competitive field in favor of larger players with greater resources, potentially reducing consumer choice and access to independent advice.

The Paradox of Protection: Does More Regulation Harm Consumers?

Here lies a profound irony. While regulation aims to protect consumers, two-thirds (67.1%) of brokers see a contradiction. Their message is clear: when advisors spend more time on bureaucracy and less with clients, the quality of advice—the true cornerstone of consumer protection—inevitably suffers. The survey asked brokers to rate the perceived value of specific regulatory areas:

| Regulatory Area | % Seeing it as Helpful/Added Value |

|---|---|

| Client Education Duties | 71.9% |

| Continuing Education Requirements | 66.9% |

| Documentation Standards | 58.4% |

| Data Protection (GDPR) | 22.5% |

| Sustainability Preference Inquiries | 12.0% |

| ESG Adjustments | 10.8% |

The data shows a clear divide. Brokers largely support rules that directly enhance their professional knowledge and client understanding. However, they are highly critical of areas perceived as overly complex, bureaucratic, or of tangential benefit to the core advisory process.

Seeking Solutions: Advocacy, Technology, and Streamlined Processes

Industry leaders recognize the urgency. Erwin Hausen, Coordinator of the BFV, states, "Regulation is important—no question. But over-regulation leads to less time for qualified consultations, which is the actual core of consumer protection." The BFV and its member companies, which include established insurer partners for brokers, are actively advocating for more pragmatic regulations with European and German legislators.

The path forward involves a dual strategy:

- Political Advocacy: Pushing for a regulatory framework that is effective without being suffocating, emphasizing that time spent with clients is the ultimate consumer protection.

- Practical Support for Brokers: Developing and promoting digital tools, streamlined processes, and targeted training to help brokers manage compliance more efficiently. Embracing technology for document management and client onboarding can reclaim precious hours.

Your Next Step: Adapting to the New Reality

For brokers feeling this pressure, the message is not to surrender but to adapt strategically. Investing in specialized compliance software, seeking out efficient back-office solutions, and aligning with network partners that offer regulatory support can be crucial survival tactics. The future belongs to brokers who can master the balance between indispensable compliance and irreplaceable personal advisory service. The industry's call for change is now backed by hard data—the question is how quickly and effectively stakeholders will respond to prevent a drain of experienced talent and a decline in advisory quality.